Medigap vs Medicare Advantage

This Is the Biggest Decision in Medicare

After enrolling in Parts A and B, every beneficiary faces the same choice: supplement Original Medicare with a Medigap plan, or replace it with a Medicare Advantage plan. Here's how to think about it clearly.

Side-by-Side Comparison

| Feature | Medigap (Supplement) | Medicare Advantage (Part C) |

|---|---|---|

| Monthly premium | Higher (~$150–300) | Often $0 |

| Doctor choice | Any doctor accepting Medicare | Network only (HMO/PPO) |

| Referrals needed | No | Often yes (HMO plans) |

| Out-of-pocket max | Effectively $0 with Plan G | $2,000–$8,300 MOOP |

| Prescription drugs | Need separate Part D plan | Usually included |

| Extra benefits | None | Dental, vision, hearing, gym |

| Prior authorization | No | Often required |

Which Path Is Right for You?

"I want predictability"

If you want to know exactly what you'll pay each month and never worry about surprise bills, Medigap (especially Plan G) is the stronger choice.

→ Choose Medigap

"I want low monthly costs"

If you're healthy, stay near home, and want extras like dental and vision without paying high premiums, Medicare Advantage can save you money.

→ Choose Medicare Advantage

"I have limited income"

Before choosing either path, check if you qualify for Medicare Savings Programs (QMB/SLMB/QI) — they can pay your premiums for you.

→ Check MSP eligibilityKey Timing: Medigap Open Enrollment

You have a 6-month Medigap Open Enrollment Period starting when your Part B begins. During this window, insurance companies cannot deny you coverage or charge more due to health conditions.

If you miss this window, you may face medical underwriting — meaning companies can reject your application or charge higher premiums based on your health history.

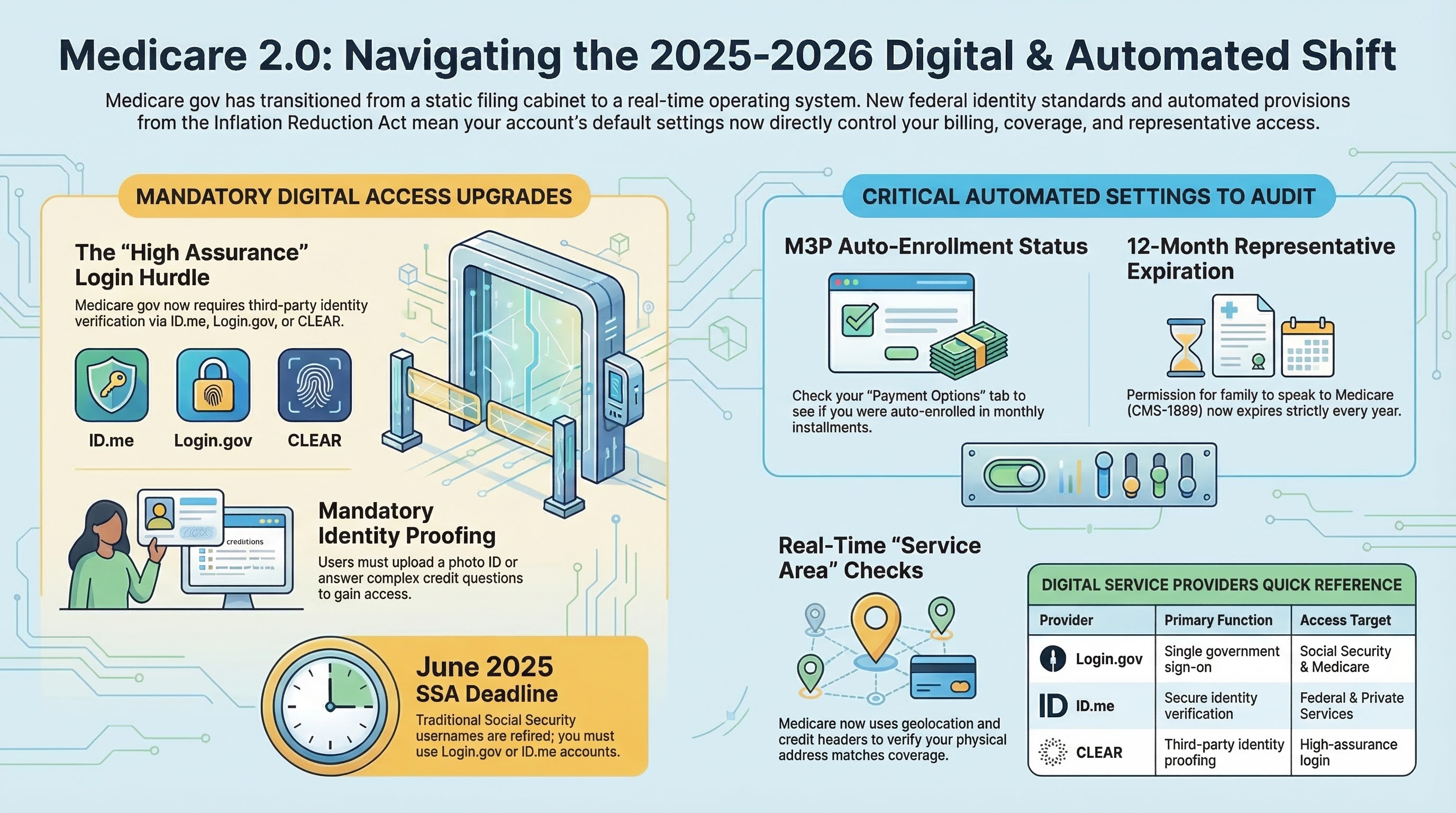

Infographic: The Medicare Digital Shift

Want to do the math with your own numbers?

Our interactive workbook helps you compare costs side by side.